The Oregon foreclosure process timeline outlines the events that unfold when a homeowner cannot meet their mortgage obligations, ultimately resulting in the unfortunate loss of their property. This timeline typically commences with the homeowner falling behind on their payments, leading to a period of delinquency. After a specific timeframe, usually around 90 days, the lender initiates the foreclosure process by formally filing a Notice of Default (NOD) with the county recorder’s office.

This NOD serves as an official notification to the homeowner that their property is now at risk of foreclosure. Following the NOD, there is a waiting period during which the homeowner can reinstate the loan or explore alternative options such as loan modification or even considering a short sale. However, if no resolution is reached during this period, the lender proceeds by filing a Notice of Sale (NOS), which sets a specific date for the property to be sold at a public auction. On the designated sale date, the property is then auctioned off to the highest bidder, often a representative from the lending institution. It is worth noting that if the property fails to sell at auction, it becomes the lender’s real estate (REO). The entire Oregon foreclosure process timeline can vary in duration but typically encompasses several months from the initial delinquency to the final sale or transfer of ownership. Suppose circumstances arise where a homeowner needs to sell their home for cash in Oregon. In that case, it is essential to understand the intricacies of the foreclosure process timeline to make informed decisions.

Understanding Oregon’s Foreclosure Laws

Understanding Oregon’s foreclosure laws is essential for anyone navigating the Oregon foreclosure process timeline. These laws outline the legal procedures and rights of the homeowner and the lender throughout the foreclosure process. Familiarizing oneself with these laws is crucial to ensure a fair and just resolution. Oregon’s foreclosure laws address various aspects, such as notice requirements, redemption periods, and the process of foreclosure auctions. By understanding these laws, homeowners can make informed decisions and take appropriate actions to protect their interests.

Whether you’re a homeowner facing the possibility of foreclosure or a potential buyer interested in purchasing a foreclosed property, having a solid understanding of Oregon’s foreclosure laws is paramount to navigating this complex process successfully.

How Foreclosure Laws in Oregon Protect Homeowners

Foreclosure laws in Oregon are designed to provide significant protection for homeowners facing the possibility of losing their homes. These laws ensure fair and transparent procedures throughout foreclosure, offering homeowners security and peace of mind. One key aspect of these laws is the requirement for lenders to provide a written notice of default to the homeowner, giving them a chance to rectify any default before proceeding with foreclosure.

Oregon law mandates a judicial foreclosure process, which means the foreclosure must go through the court system, allowing homeowners to present their case and potentially halt the foreclosure. This aspect of the law offers a safeguard against hasty or unjust foreclosures. Furthermore, Oregon has implemented a redemption period, providing homeowners with the opportunity to reclaim their property even after the foreclosure sale has taken place. These protective measures, combined with the meticulous timeline of the Oregon foreclosure process, work together to safeguard homeowners and ensure that their rights are preserved throughout the challenging foreclosure experience.

The Role of the Oregon Revised Statutes in the Foreclosure Process

The Oregon Revised Statutes play a crucial role in the foreclosure process within Oregon. These statutes are a comprehensive set of laws outlining the legal procedures and requirements to be followed when a property owner faces foreclosure. They provide a framework for both the lender and the borrower, establishing the rights and responsibilities of each party involved.

The Oregon Revised Statutes cover various aspects of the foreclosure process, including notice requirements, timelines, and steps to initiate and complete a foreclosure. These statutes ensure that the foreclosure process is fair and transparent, protecting the rights of both parties and providing a clear legal framework for resolving foreclosure cases. Understanding and adhering to the Oregon Revised Statutes is essential for all parties involved in the foreclosure process to ensure compliance with the law and a fair outcome for all.

Other Articles You Might Enjoy

- What Does Pre Foreclosure NOD Mean

- Pre-foreclosure meaning

- Can a Nursing Home Take Your House in Oregon?

- Can Police Remove Squatters in Oregon

- Are There Squatters Rights In Oregon?

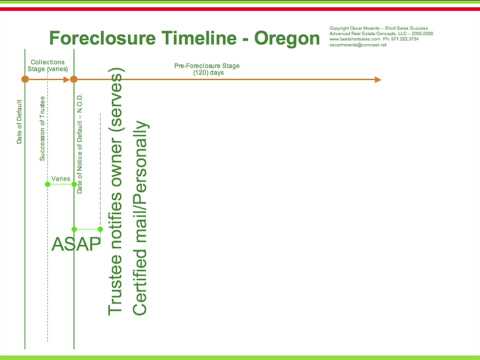

The Timeline of the Foreclosure Process in Oregon

The foreclosure process in Oregon follows a specific timeline that can be complex and daunting for homeowners facing financial difficulties. Understanding this timeline is crucial for those seeking to navigate the process and potentially avoid losing their homes. The first step in the Oregon foreclosure process is issuing a Notice of Default (NOD) by the lender to the borrower, indicating that the borrower is in default of their mortgage obligations. Following this, a period of 120 days is provided for the borrower to cure the default by bringing the mortgage payments up to date. If the borrower fails to cure the default within this timeframe, the lender may proceed with filing a Notice of Sale (NOS), which sets a date for the foreclosure auction.

The NOS must be published in a local newspaper for at least four consecutive weeks before the auction date. On the scheduled auction date, the property is sold to the highest bidder, typically the lender and a Trustee’s Deed is issued to transfer ownership. It is important to note that Oregon allows for a redemption period after the foreclosure sale, during which the borrower has the right to reclaim the property by paying the total amount owed plus any additional costs. The foreclosure process timeline in Oregon can vary depending on various factors, such as legal proceedings and negotiations between the borrower and lender, making it essential for homeowners to seek legal advice and explore available options to mitigate the consequences of foreclosure.

Initial Steps in Oregon’s Foreclosure Process

The initial steps in Oregon’s foreclosure process are critical for homeowners possibly losing their properties. Understanding these steps is essential for navigating the complex and often confusing process. The first step is typically the issuance of a Notice of Default by the lender, which informs the homeowner that they have defaulted on their mortgage payments. This notice outlines the amount owed and provides a specific timeframe for the homeowner to remedy the default.

Homeowners need to take immediate action upon receiving this notice to explore potential options such as loan modification or refinancing. Failure to address the default within the specified timeframe may lead to the next step in the process: filing a Notice of Sale. This notice sets a date for the public auction of the property, allowing interested parties to bid on it. Homeowners should seek legal advice at this stage to understand their rights and explore potential alternatives to foreclosure. By taking these initial steps, homeowners in Oregon can better navigate the foreclosure process and potentially find a solution that allows them to retain their homes.

Call Now (818) 651-8166

Why Sell Your Home to ASAP Cash Offer?

- You Pay Zero Fees

- Close quickly 7-28 days.

- Guaranteed Offer, no waiting.

- No repairs required, sell “AS IS”

- No appraisals or delays.

What Happens After the Notice of Default in Oregon

After the Notice of Default is issued in Oregon, the homeowner enters a critical stage in the foreclosure process. This notice serves as a warning that the borrower has fallen behind on their mortgage payments, and if they fail to take action, their property may be sold at a public auction. At this point, the homeowner has a few options to consider. One option is to reinstate the loan by paying all outstanding amounts, including late fees and penalties. Another option is negotiating a loan modification with the lender, which can help make the payments more manageable.

The homeowner may sell the property through a short sale, using the proceeds to satisfy the debt. If none of these options are pursued, the foreclosure process will continue, leading to the sale of the property at a public auction. Homeowners must act promptly and seek professional guidance to navigate this challenging phase and explore the best possible outcome.

Preventing Foreclosure in Oregon

If you face the possibility of foreclosure in Oregon, it is crucial to understand the steps you can take to prevent this distressing outcome. The Oregon foreclosure process timeline provides a framework for navigating this challenging situation. By familiarizing yourself with the various stages, such as the initial notice of default, the mediation period, and the sale of the property, you can better comprehend the options available. One effective strategy for preventing foreclosure in Oregon is seeking assistance from reputable foreclosure prevention agencies or housing counseling services.

These professionals can guide you through the complexities of the process, offering valuable advice on negotiating with lenders, exploring loan modification options, or pursuing alternatives like short sales or deeds instead of foreclosure. Additionally, it is essential to stay informed about the eligibility criteria for foreclosure prevention programs, such as the Oregon Foreclosure Avoidance Program (OFAP), which offers financial assistance to eligible homeowners. By proactively taking steps to prevent foreclosure and leveraging the resources available to you, you can strive to protect your home and financial stability.

Other Articles You Might Enjoy

- Ohio Foreclosure Process Timeline

- North Dakota Foreclosure Process Timeline

- New York Foreclosure Process Timeline

- North Carolina Foreclosure Process Timeline

- New Jersey Foreclosure Process Timeline

Practical Strategies to Avoid Foreclosure in Oregon

If you face the challenging situation of potential foreclosure in Oregon, it is crucial to know practical strategies to help you avoid this outcome. One critical step is to communicate openly and promptly with your lender, as they may be willing to work with you to find a solution. Exploring loan modification options, such as requesting a lower interest rate or extending the repayment period, can also be beneficial. Seeking assistance from a housing counseling agency can provide valuable guidance and support. Another approach to consider is refinancing your mortgage, which could potentially lower your monthly payments.

Furthermore, exploring alternative sources of income or reducing expenses can help you manage your finances more effectively and improve your ability to meet your mortgage obligations. It is important to remember that each situation is unique, and consulting with a qualified attorney or financial advisor can provide personalized advice based on your specific circumstances. Taking proactive measures and implementing these practical strategies can increase your chances of avoiding foreclosure and finding a favorable resolution.

How Oregon’s Foreclosure Mediation Program Works

Oregon’s Foreclosure Mediation Program is designed to allow homeowners to resolve their foreclosure concerns through mediation. This program, part of the broader Oregon Foreclosure Process Timeline, aims to create a fair and balanced environment for homeowners and lenders to negotiate potential solutions. The program begins when a homeowner receives a Notice of Default, triggering 30 days for them to request mediation. If the homeowner submits a timely request, the foreclosure process is temporarily paused while mediation occurs.

During the mediation session, a neutral mediator facilitates discussions between the homeowner and the lender to reach a mutually agreeable resolution. This can include loan modifications, repayment plans, or other alternatives that help the homeowner avoid foreclosure. If an agreement is reached, it is documented in a written agreement and becomes binding on both parties. However, if no resolution is reached, the foreclosure process resumes. It is important to note that participation in the mediation program does not guarantee a favorable outcome. Still, it allows homeowners to explore options and find a way to keep their homes.

Call Now (818) 651-8166

Why Sell Your Home to ASAP Cash Offer?

- You Pay Zero Fees

- Close quickly 7-28 days.

- Guaranteed Offer, no waiting.

- No repairs required, sell “AS IS”

- No appraisals or delays.

Life After Foreclosure in Oregon

Life After Foreclosure in Oregon can be a daunting and uncertain journey for individuals and families who have experienced the unfortunate event of losing their homes. The Oregon Foreclosure Process Timeline adds more complexity to this already challenging situation. However, it is essential to note that life does not end after foreclosure. There are options and resources available to help navigate the aftermath and regain stability. One key aspect to consider is financial recovery. It may take time to rebuild credit and secure a new living place, but it can bounce back with perseverance and proper guidance. Seeking professional advice from experienced counselors or organizations specializing in post-foreclosure assistance can provide valuable insights and support during this transitional period.

Exploring alternative housing options, such as renting or exploring government assistance programs, can help individuals and families find a new place to call home. Emotionally, the process of moving on after foreclosure can be challenging. It is important to remember that experiencing foreclosure does not define a person or their worth. Connecting with support groups or seeking counseling services can assist in healing and rebuilding self-esteem. Life after foreclosure in Oregon may present challenges, but it also offers opportunities for growth, resilience, and a fresh start.

Rebuilding Your Credit Post-Foreclosure in Oregon

Rebuilding your credit after experiencing foreclosure in Oregon can be challenging, but it is possible to regain financial stability with the proper steps and mindset. The Oregon foreclosure process timeline can vary depending on various factors, such as the type of foreclosure and the specific circumstances. Once the foreclosure process is completed, it is essential to take proactive measures to rebuild your credit. Start by obtaining a copy of your credit report to assess the damage and identify any discrepancies.

Next, focus on paying your bills on time and in full to demonstrate responsible financial behavior. Consider applying for a secured credit card to help establish a positive payment history. Additionally, seek out reputable credit counseling agencies in Oregon that can provide guidance and support in managing your finances effectively. Remember, rebuilding your credit takes time and patience, but with persistence and the right strategies, you can gradually improve your creditworthiness and regain control of your financial future.

Finding Housing After Foreclosure in Oregon

Finding housing after foreclosure in Oregon can be a challenging and overwhelming process. The Oregon foreclosure process timeline adds complexity to this already difficult situation. However, finding suitable housing options with careful planning and research is possible. One crucial step is to understand the various resources available to individuals who have experienced foreclosure. Local housing agencies, such as the Oregon Housing and Community Services, provide assistance programs and resources to help individuals find affordable housing options.

Exploring rental listings and contacting property management companies can increase the chances of finding available rentals. It is also recommended to work on rebuilding credit and saving for a down payment, as these factors can positively impact the ability to secure housing after foreclosure. Overall, navigating the process of finding housing after foreclosure in Oregon requires perseverance, resourcefulness, and utilizing the available assistance programs and resources.

{kind=link}